The Month in Review - Oct 2019

Monthly Review

Farrow Hughes Mulcahy Investment Research 07 November 2019

During October the Australian market was down around 0.4%. World markets rallied rising just over 2% in $US terms.

On the global side, forward-looking indicators such as the ISM manufacturing index demonstrate that uncertainty over trade and policy continues to weigh on sentiment. However, co-incident indicators – such as the US payroll data released on Friday – are coming in stronger than many expected. The risk is that weaker sentiment does start to change corporate behaviour, feeding through to weaker employment in the US. However, as we stand today the environment is broadly supportive for equities. There is reasonable growth, but not strong enough to switch the Fed from its easing bias. Outside the US the Chinese ISM was also slightly better than consensus expectations.

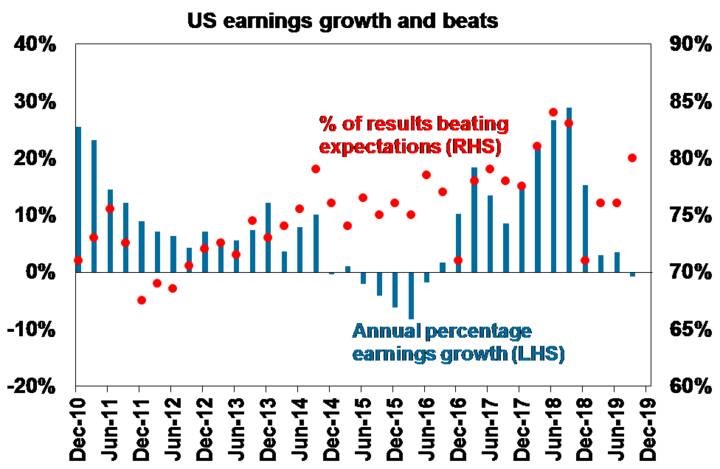

US September quarter earnings results remain reasonable. About 70% of S&P500 companies have now reported, with 80% beating earnings expectations (against a norm of 75%) by an average of 5.2% and 61% beating on sales. Earnings growth over the last year looks likely to end up with a small gain, but this is better than market expectations at the start of the reporting season which saw a 3% decline.

While Australian inflation remained very low in the September quarter our expectation is for further rate cuts next year. September quarter inflation was 1.7% year on year with the average of the core measures at 1.4% year on year. This was soft but looks unlikely to move the RBA to ease next month following recent comments by RBA Governor Lowe suggesting greater confidence in a “gentle upturn” in the economy and patience in getting inflation back to target all of which suggests the RBA is in little hurry to cut rates just yet. However, we remain of the view that further RBA monetary easing will be required and is likely. Growth is likely to remain subdued and below trend for longer than the RBA is allowing. This will keep unemployment higher for longer and wages growth and inflation below target for longer.

October has already seen the $A rise by more than 3% which is a defacto monetary tightening and is the last thing the economy needs. So, in the absence of more fiscal stimulus, pressure remains on the RBA for further easing.

Australian economic data was a mixed bag. Home building approvals rose in September, but this was due to a bounce in volatile unit approvals with the fall in dwelling approvals over the last year pointing to further weakness in home building construction over the next six months or so. Fortunately, this will be partly offset by non-residential building where approvals have been trending up solidly and unit approvals look like they may be stabilising. But the bottom line seems to be that the economy is still growing but remains constrained.

Share markets remain at risk of further short-term volatility given issues around trade, Iran & the Middle East, impeachment noise and weak global economic data. But valuations are okay – particularly against low bond yields, global growth indicators are expected to improve by next year and monetary and fiscal policy are becoming more supportive all of which should support decent gains for share markets on a 6-12 month horizon.

Low yields are likely to see low returns from bonds once their yields bottom out, but government bonds remain excellent portfolio diversifiers.

The election outcome, rate cuts, tax cuts and the removal of the 7% mortgage rate test are driving a rebound in national average capital city home prices led by Sydney and Melbourne. But beyond an initial bounce, home price gains are likely to be constrained through next year as lending standards remain tight, the record supply of units continues to impact and rising unemployment acts as a constraint. The risk though is that the recent surge in prices goes on for longer as property price gains in Australia have a habit of feeding on themselves.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 0.25% by early next year.