The Australian market managed to finish with a gain of about 1% for May thanks largely to a sharp rally post the re-election of the Liberal government. International markets declined on average about 6% for the month.

Trade war fears continued to ramp up over the past week with President Trump saying he was “not yet ready” to make a deal with China and hints from China that it may stop exports of rare earth minerals to the US and reports that it will set up a blacklist of firms that hurt Chinese interests highlighting that the dispute is moving beyond tariffs and Trump opening a new tariff front with Mexico. China supplies around 80% of US rare earth imports and they are essential in sectors like defence and electronics. The US could retaliate by banning the sale of semiconductor chips to China. Clearly this ongoing escalation is not good for business confidence, growth and profits. Share markets are likely to have to fall a lot further to make President Trump realise just how great the threat to the US economy and by implication his 2020 re-election prospects are (US Presidents don’t get re-elected when unemployment is rising). So, shares likely face more short-term downside as the trade conflicts will likely get worse before they get better. The “great negotiator” (President Trump) surely realises that he won’t look so great if all he has to show for his trade wars is rising unemployment.

US consumer confidence rebounded in May and remains solid highlighting that while the trade war is impacting business confidence it’s not yet having much impact on consumers. In particular, consumer perceptions of the jobs market remain very strong which is consistent with jobless claims remaining ultra-low. Consistent with this, April data for personal spending was solid. Meanwhile, housing data remains mixed with pending home sales down in April and flat on a year ago and house price growth slowing but lower mortgage rates should help.

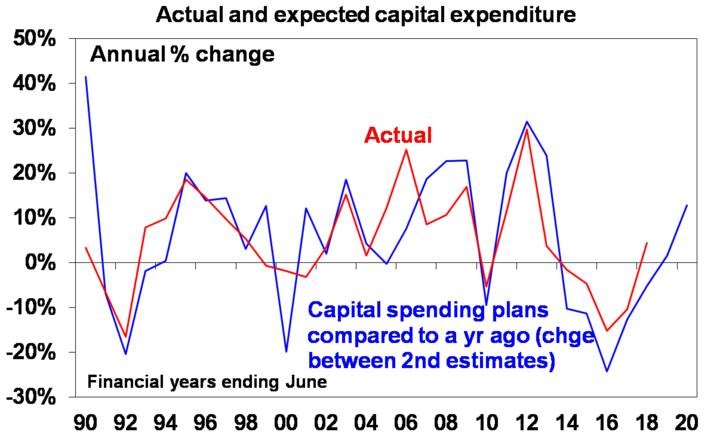

Australian data was generally soft over the last week with a further fall in building approvals, broad based declines in business investment and continuing soft credit growth. There was some good news though with rising business investment plans for 2019-20 as the mining investment bust bottoms out and turns up and as non-mining investment continues to head up. Weak demand growth in the economy will probably mean that it won’t be anywhere near as strong as the next chart implies though.

Source: ABS, AMP Capital

The minimum wage to rise 3% from July - but that’s less than last year’s 3.5% rise. With around 20% of the workforce (those on awards) getting the minimum wage rise it actually implies a 0.1% pa fall in overall wages growth over the year ahead (ie from 2.3% year on year down to around 2.2% yoy) all else equal. Expect wages growth to remain soft!

The combination of slower growth in the minimum wage, falling building approvals, soft credit growth, falling March quarter investment and likely only modestly rising capex in 2019-20 leave the RBA on track to cut rates on Tuesday by 0.25% with further cuts to follow.

Share markets are likely to see a further pull back in the short term on the back of uncertainty about trade and mixed economic data. But valuations are okay, global growth is expected to improve into the second half if the trade issue is resolved and monetary and fiscal policy have become more supportive of markets all of which should support decent gains for share markets through 2019 as a whole.

National average capital city house prices are likely to remain under pressure from tight credit, record supply and reduced foreign demand. However, the combination of imminent rate cuts, support for first home buyers via the First Home Loan Deposit Scheme, the relaxation of the 7% mortgage rate serviceability test and the removal of the threat to negative gearing and the capital gains tax discount point to house prices bottoming out by year end.

Cash and bank deposits are likely to provide poor returns as the RBA may cut the official cash rate to 1% by year end.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.