The Month in Review - Jun 2019

Monthly Review

Farrow Hughes Mulcahy Investment Research 02 July 2019

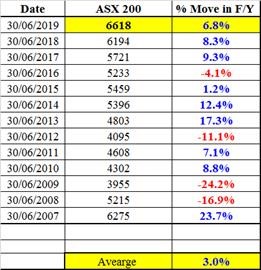

The Australian market managed to finish the financial year with a gain of 6.8%. With dividends added it comes to about 11%. At the same time The MSCI world index in US dollars was up 4.2%.

It is worthwhile spending some time to put the Australian returns in perspective.

ASX 200 was up +6.8%, which was;

1.below last year's (2017/2018) rise of +8.3%

2.and also below the year before that (2016/2017) when we had a +9.3% return

3.BUT better than 3 years ago when we had negative return in 2015/ 2016 (i.e. where it fell -4.1%).

So you could say it’s the 3rd best in the last 4 years.

ASX 200 - is finally - for the 1st time in 12 years now above where it was 12 years ago!!

But it is also the highest (record) close for a Financial Year ...

•The ASX 200 is now at 6618 vs 6275, i.e. about +5.5% above where it closed 12 years ago (on 30th June 2007 i.e. 6275).

So in 12 years the ASX 200 - is now finally back above where it was 12 years ago - but also at record high (for the end of a F/Y)

•Table shows ASX 200 returns in last 12 Financial years + 2019.

Source: Coppo Report.

Looking at the ASX 200 in the previous 25 Financial Years (not including this year)

•Still over the previous 26 years we have only had 7 negative Financial Years.

•So 73% of the time the market closes higher for the F/Y.

The average move in the ASX 200 over those 26 years has been +5.89%.

•While in the 19 up years (3/4 of the time) the average rise had been a healthy +11.84%

•But the 7 negative years (1/4 of the time) have had an average fall of a nasty -10.24%

Table of all Financial Year Returns ASX 200 (XJO) for the last 26 years

Source: Coppo Report.

On balance, the backdrop for equity markets remains positive. In the US, investor sentiment was improved by the Fed’s latest announcement that every US-listed major bank had passed their annual stress test, which saw the big banks subsequently commit themselves to returning $136b of combined capital to shareholders over the next 12 months.

Over the weekend, we also had some positive updates from the G20 summit in Osaka: a truce, or at least a temporary reprieve in the US-Sino trade tensions was achieved by Trump and Xi, alleviating (somewhat) concerns around the outlook for global economic growth. Both parties have returned to the negotiating table, with the US agreeing to halt additional tariff hikes for now, and China in exchange will buy more agricultural products from the US immediately. In addition, US companies are also allowed to sell components again to the world’s largest telecommunications equipment manufacturer, Huawei. The Chinese telecom giant has been near the epicentre of the trade talks.

Also at the global macro level, another key agreement achieved at the summit was between Russia and Saudi Arabia, extending their current production curtailment by another six to nine months.

While the OPEC+ is yet to meet (early this week) this agreement is very likely to be adopted by the rest of the countries in the alliance. While remaining below the highs achieved in April, Brent crude has come back a fair way over the latter part of June, up ~10% to US$66.55/bbl by the end of last week.

Share markets remain vulnerable to short term volatility and weakness on the back of uncertainty about trade, Middle East tensions and mixed economic data. But valuations are okay – particularly against low bond yields, global growth indicators are expected to improve into the second half if the trade issue is resolved and monetary and fiscal policy is likely to become more supportive, all of which should support decent gains for share markets over the next 6-12 months.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.