The Month in Review - November 2018

Monthly Review

Farrow Hughes Mulcahy Investment Research 06 December 2018

The S&P/ASX 200 index fell 2.2% in November whilst the MSCI World Index (AU) also fell by 1.8%.

The past week and most notably events around the weekend G20 summit in Buenos Aires saw some positive developments for shares and risk assets that provide more confidence that shares will see a rally into year-end and that we won’t go into a major (“grizzly”) bear market. First, comments from Fed Chair Powell and Vice-Chair Clarida along with the minutes from the last Fed meeting have added confidence to the prospect of a pause in rate hikes next year. The key message from the Fed is that it remains upbeat on the US economy – consistent with another hike in December, but that rates are now "just below…neutral" and it needs to be aware of potential headwinds to growth including the lagged response in the economy to past monetary tightening and that there are no major excesses to deal with, which is all consistent with the Fed being open to a pause and slower pace of rate hikes next year.

Second, the meeting at the G20 summit between President Donald Trump and President Xi Jinping has gone well with both describing it as “highly successful.” Basically, the US and China have agreed to halt the imposition of new tariffs (including the scheduled January 1 increase from 10% to 25% on $US200 billion of US imports from China) for 90 days as the two countries negotiate a lasting agreement to solve their differences around trade and other issues. This is a short-term positive for markets as it’s more than most appear to have been expecting from the meeting. Of course, it makes March 1 next year a bit of a drop-dead date (yet another one!) and it could still end in failure like the other attempts at negotiation so far this year. However, there are some big positives this time around pointing to a more successful end to these negotiations which would be positive for investment markets next year. China has indicated a preparedness to negotiate on issues like forced technology transfer, intellectual property protection and cyber intrusions that it hasn’t before.

Thirdly, the fact that the G20 leaders’ summit at least agreed on a communique unlike the G7 and APEC summits is a good sign that compromise can be found around the trade issue that results in a stronger trading system as opposed to a descent into trade wars.

Finally, while the 30% or so slump in the oil price will provide a boost to consumer spending power and hence growth, confirmation from Saudi Arabia and Russia at the G20 summit that they plan to extend their agreement into next year to manage the world oil market is consistent with an agreement to cut back oil production (which is likely to be confirmed at this Thursday’s OPEC meeting), which will provide confidence that a re-run of the 2014-16 75% oil price crash won’t be repeated, which should provide some relief for energy stocks and support for energy related investment.

In Australia a stronger budget position likely to see the Government announce tax cuts ahead of next year’s Federal election. PM Morrison’s announcement that next year’s budget will be brought forward to April 2 is clearly designed to clear the way for an election in May (on either May 11 or May 18). Meanwhile, the Mid Year Economic and Fiscal Outlook report to be delivered on December 17 is likely to show the Federal budget is running around $9 billion per annum better than expected, thanks to higher than expected commodity prices and employment driving stronger tax revenue only partly offset by fiscal easing measures.

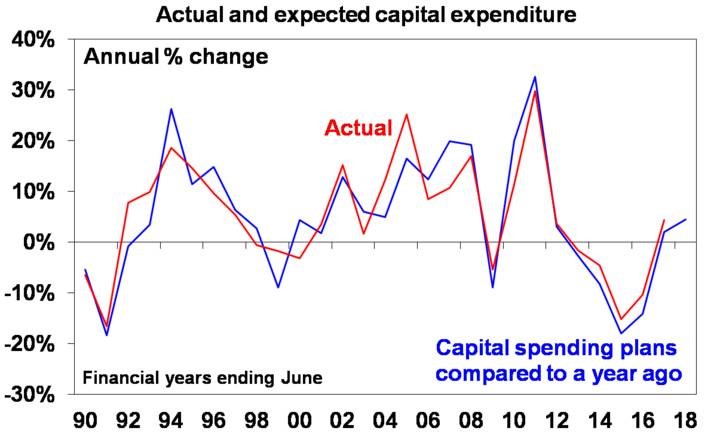

Australia data released over the last week was messy, with a sharp fall in September quarter construction activity that was broad-based across residential and non-residential building and engineering activity, a fall in September quarter private new capital expenditure and continuing softness in credit growth. There was good news though in that business investment plans for the current financial year continue to improve, with capital spending plans compared to a year ago growing at their fastest in six years as the slump in mining investment slows but non-mining investment improves. So, business investment should help provide an offset to the downturn in the housing cycle.

Source: ABS, AMP Capital

Shares remain at risk of further short-term weakness, but we continue to see the trend in shares remaining up as global growth remains solid helping drive good earnings growth and monetary policy remains easy.

National capital city residential property prices are expected to slow further with Sydney and Melbourne property prices likely to fall another 15% or so, but Perth and Darwin property prices at or close to bottoming, and Hobart, Adelaide, Canberra and Brisbane seeing moderate gains.

Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.2%.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

We’d like to take this opportunity to wish all of our clients and their families a Merry Christmas and a safe and profitable 2019.